Some of our forum members have been asking whether there are other alternative financial instruments for them to preserve some more of their savings and capital either for a future business or to address particular medium-term goals.

Remember that in any type of investment, there are advantages and disadvantages. Make sure that you have identified the risks and are willing to take such risks.

So what are some examples of low-risk and affordable investment options that risk-averse Filipino investors may put some of their cash in? Read on.

1) High-Yield Time Deposits

While there are Philippine banks that offer great interest rates most of them require a large minimum placement. And then some banks that offer higher interest rates and affordable minimum placements are either new in the industry or have no major investments and assets to back them up.

And while the Philippine inflation rate is at 3.3%, average retail investors may consider saving their extra money in these 5-year term deposit products that guarantee to give 3.75% to 5.5% annual interest which is compounded monthly if not withdrawn within 5 years.

Furthermore, this type of time deposit is tax-free when not withdrawn before maturity period. They are also insured by the PDIC for up to 500,000 for each depositor.

(Note: Invest only the money you won’t need in the next 5 years in this instrument.)

You may check out the following banks for these high-yield term deposit products:

Malayan Bank’s Growth Saver – Guaranteed 5.5% interest per annum with a minimum monthly deposit of P1,000 for 5 years.

Philippine Veterans Bank’s Hyper Saver and Maxi-Return – This is for those with at least P100,000 cash on hand or savings and are hoping to maximize their returns in the next 5 years.

Plantersbank Premium 5 – A 5-year term deposit with a minimum placement of P50,000 with free insurance up to P1 million.

You may also inquire from other banks about similar term deposit products.

2) Long Term Negotiable Certificate of Deposit or LTNCD’s is bank product with higher interest rate compared to a short-term time deposit product.

These are similar to high-yield long term time deposits as they both have 5-year maturity dates and fixed interest rates. It is also exempted from paying the 20% withholding tax charged on savings or time deposit accounts.

And since it is a bank product, it is also insured by the PDIC for up to 500,000 for each depositor. However, LTNCD’s can not be preterminated unlike time deposits. That means an investor has to wait for 5 years before he can withdraw the principal.

An alternative solution is to sell an LTNCD to a willing buyer since this instrument, as the name suggests, is negotiable or tradable. Check out major banks such as BDO, Landbank, Unionbank, EastWest, PNB, RCBC, Security Bank, Metrobank, UCPB, etc. for LTNCD’s that they are issuing to the public.

Interests start from 3.5% per annum up 5.85% per annum that are usually paid quarterly and are tax-exempt for individual investors who hold the LTNCDs for at least five years.

(Save and grow your money while you are still an OFW!!! CLICK here!)

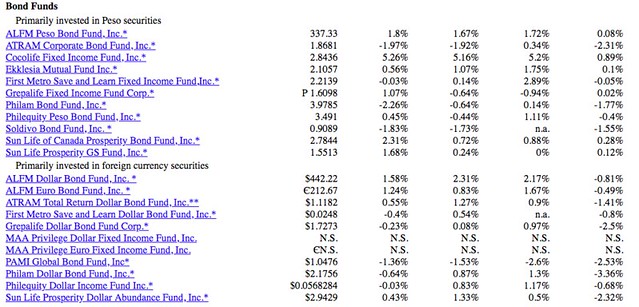

3) Fixed Income Mutual Funds or UITF’s (Unit Investment Trust Funds)

Bond funds and other fixed income funds offered by mutual fund companies (for mutual funds) and banks (for UITF’s) are great options for risk averse retail investors.

The illustrations below show the performance of bond mutual funds courtesy of Philippine Investment Funds Assocation or PIFA. NAVPS Performance is as of March 6, 2018.

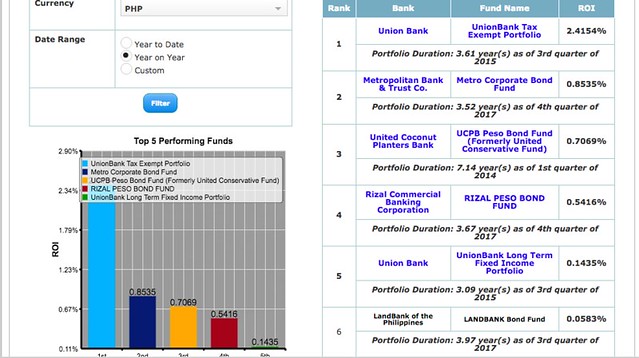

Fixed income UITF’s or unit investment trust funds work similarly as bond/fixed income mutual funds. There are few differences that we discussed in our previous article about mutual funds and UITF’s.

Below shows the data of Philippine UITF’s NAVPU performance as March 6, 2018 c/o www.uitf.com.ph.

Long-term Bond UITF’s

4) Preferred Stocks

Philippine blue chip companies such as Ayala Corporation, Security Bank, San Miguel, First Gen, among others offer preferred stocks to the public. Companies do this basically to raise funds for business expansion. These are offered with a promised fixed return.

One good example is Ayala Corporation’s Class B Preferred Shares which was issued at a maximum price of P500 per share. You should have at least P50,000 since the minimum number of shares you can purchase is 100. The shares that investors purchased will pay a dividend rate of around 4.75 to 5.5% per year.

Other companies may offer lower fixed dividend rates.

Stock investors already trading with common shares are offered by stockbrokers to buy these preferred shares. You can open a stock trading account with any PSE-registered stockbrokers if you want to avail these. Others can invest through these companies’ underwriters which are usually some of the major banks in the country.

Other Fixed Income Instruments

There are other low-risk investment options that retail investors and any individual can invest in. These are corporate bonds, treasury bills, treasury notes, municipal bonds, retail treasury bonds, shares from cooperatives, rural bank bonds, housing bonds, and other government bonds.

Most of these don’t offer interests or returns that are higher than inflation rate these days but will definitely provide you with extra passive investment class in your portfolio.

PAG-IBIG’s MP2 Program and other similar savings programs offered by the government may also be considered as an additional placement for your extra money.

Instruments such as variable unit-linked insurance products can also be great options for you.

As a final reminder, investors should always take a closer look first and analyze the investment vehicle being offered to them before entrusting their money to brokers or fund managers.

Study first before investing.

UPDATE: San Miguel Corp. is offering up to Php30 billion worth of fixed-rate retail bonds split across three series with varying maturity dates and interest rates.

Investors can choose between five-year bonds with an annual return of 6.25%; seven-year bonds with an interest rate of 6.625% per annum; and 10-year bonds that have an annual coupon rate of 7.125%.

Interested investors are encouraged to read San Miguel’s offer supplement for more information.

Continue to receive more information about financial instruments and investment vehicles by subscribing to RockToRiches|burngutierrez.com for FREE.

If you want me to coach you in improving your finances, type your name and email below and click the Subscribe button:

Rock your way to abundance!

— —

— —

If you want me to coach you in improving your finances, type your name and email below and click the Subscribe button:

========

Do you automatically zone out at the mere mention of investments, insurances, and options for retirement?

Financial literacy is such an important topic, so we made it a more fun and digestible read in my latest book, #MoneyTroubleShooters!

Read more about the book here ➡️ http://moneytroubleshooters.com/about/

any advice in getting VUL with 100% equity bonds? thanks

This may help you: http://moneyfacts.co.uk/guides/investments/guaranteed-equity-bonds/ If it fits your risk profile and financial goal, then go for it.

Choose a VUL company that has the highest annual return in their investments. I’m a Financial Consultant myself, please contact me if you have more questions. Thanks

bro burn, pag sinabi mong 5 year return of 9.20%, ibig sabihin gain ka ng average of 9.20% every year on a 5 year bracket?

Bob, 9.20% is the return on the 5th year only.

So that would mean an average of less than 2% per year on the 5 year period? Is that right?

Not that way Abe. Simple averaging will not be accurate in this case. You need to get the annualized returns first for investment vehicles that have compounded returns such as UITF’s.

For example, Unionbank’s intermediate-term bond UITF has the 1-year (7.8%), 3-year (6.25%), and 5-year (9.20%) returns in the illustration. But let’s assume that those are 1-year, 2-year, and 3-year returns instead.

To compute for the annual compounded return, add 1 first to each annual return, which gives us 1.078, 1.0625, and 1.0920, respectively. Then multiply them together and raise the product to the power of one-third to adjust for the fact that returns were combined from three periods.

This should give us:

(1.078)*(1.0625)*(1.0920)^1/3 = 1.077217

Subtract the 1 then multiply by 100. This shows that the fund earned 7.73% annually over the three-year period.

Hope this helps.

How to avail of the preferred stock, for example, Ayala corporation. TIA

Bro where can I avail small amount of stock.

Joel, first you need to open a stock trading account with a stockbroker, preferably online. You can check out the list of stockbrokers at http://www.pse.com.ph

Sir, which among the.bank you mention is 3.75% to 5.5% annual intetest COMPOUNDED MONTHLY if stays in 5 yrs? is the bank you recommend?

is the bank you mention you recommenf

Hi Jeanette, check out the banks I mentioned above for LTNCDs.

ThaNk you! will check those banks!

Sir please explain what is a stock warrant and how it works….

Thanks, Paul

Hi Sir,

When you say guaranteed 5.5% interest per annum, does this mean it will stay at 5.5% even if the market/economy is down? Thank you!